Personal Money Management

Personal Money Management refers to balancing one’s wealth and income with their financial essentials, desires, and plans. Though some of us may survive without sophisticated money management strategies, we cannot escape financial pressures entirely. Most of us have jobs during our most productive adult years, and the income we bring in must be managed effectively to satisfy our basic needs and lead fulfilling lives. The decisions we make regarding our finances can be complicated, and they vary as we pass through the various phases of life. We may start our adult lives simply by depositing our earnings in bank accounts and spending most or all of that income using cash and credit cards. However, as our financial needs grow, we learn how to manage our finances through other methods such as loans, debt, savings, and investing.

Personal financial management is a challenging and continuous task that causes even the most financially clever individual to become confused or short-sighted. We will discuss some tips about personal money management and the best ways to invest your money

Some tips on personal money management:

• Learn the skill of budgeting

Budgeting is one of the most important skills for managing money successfully, as it helps you identify your needs and then determine the best ways to spend this money. Many people lack this skill, which makes them unable to correctly identify their needs and thus increase their expenses significantly and thus feel constantly financially threatened.

• Stick to your monthly spending budget

Individuals must adhere to their budgets, reconcile their financial situations, and spend them according to what is available to them, while adjusting the way they spend accordingly, for example, if an individual notices that the budget for food from abroad is almost coming to an end, he should look for a less expensive restaurant or make food at home instead of exceeding the budget.

• Make your debt a priority

There is no doubt that debt is a weight on humans and affect the process of good financial planning due to the feeling of constant pressure, so it is preferable for a person to be careful not to incur debts, and if he cannot there are many ways to get rid of debts as soon as possible, including:

1- Review the current budget and try to reduce the value of some items temporarily, to try to cover part of the debt.

2- Monitor your valuable assets that are unused and useless for you to think about selling them and paying off the debt or part of it with it.

• Use installments but with caution

The installment feature is a real temptation for people to buy many products, as it poses a clear risk to the management of money and the budget mainly, so controls and a certain amount of budget must be set for installments and be for more necessary things.

• Develop yourself in the world of finance and investment and seek expert advice

To be able to maintain and manage your money well, you must use it correctly, so it is better to try to understand the world of money. It does not respond to the calls for quick and high income that have recently spread on social media sites because they are often scams. Finally, do not hesitate to seek advice from experts in this field, instead of making an unsound decision, and do not rush to make investment decisions, when it comes to money, you must be careful and not rushed, and focus on making the best decisions.

Rule 50-20-30

It is one of the effective ways of dividing and preparing the monthly budget because it helps individuals manage their monthly income with ease.

The 50-20-30 rule is based on the creation of a budget distributed as follows:

50% on basic expenses: Half of the salary is allocated to basic needs which include bills, rent, car premium, insurance, food, healthcare, and minimum debt payment.

20% for savings and investment: Upon receipt of the salary, 20% of it is deducted for saving, investment, or both, such as depositing a certain amount in a bank savings account or paying off some debts that reduce the interest due on future payments.

30% for flexible and variable expenses: These are the amounts associated with entertainment and pleasure in a complementary and not necessary sense. Such as dining in restaurants, buying tickets to sporting events, buying a new bag, buying the latest electronic devices. Flexible and variable expenditure percentages and basic expenses are the maximum as they cannot be exceeded, and the more you succeed in reducing spending ratios, the higher the chance of achieving other financial goals. The method of applying the rule after receiving the salary is divided according to the above method and the distribution of amounts according to goals and priorities, for example, if you see that the flexible expenses are greater than the percentage allocated to them, you reduce them or dispense with some of them to adjust the rule.

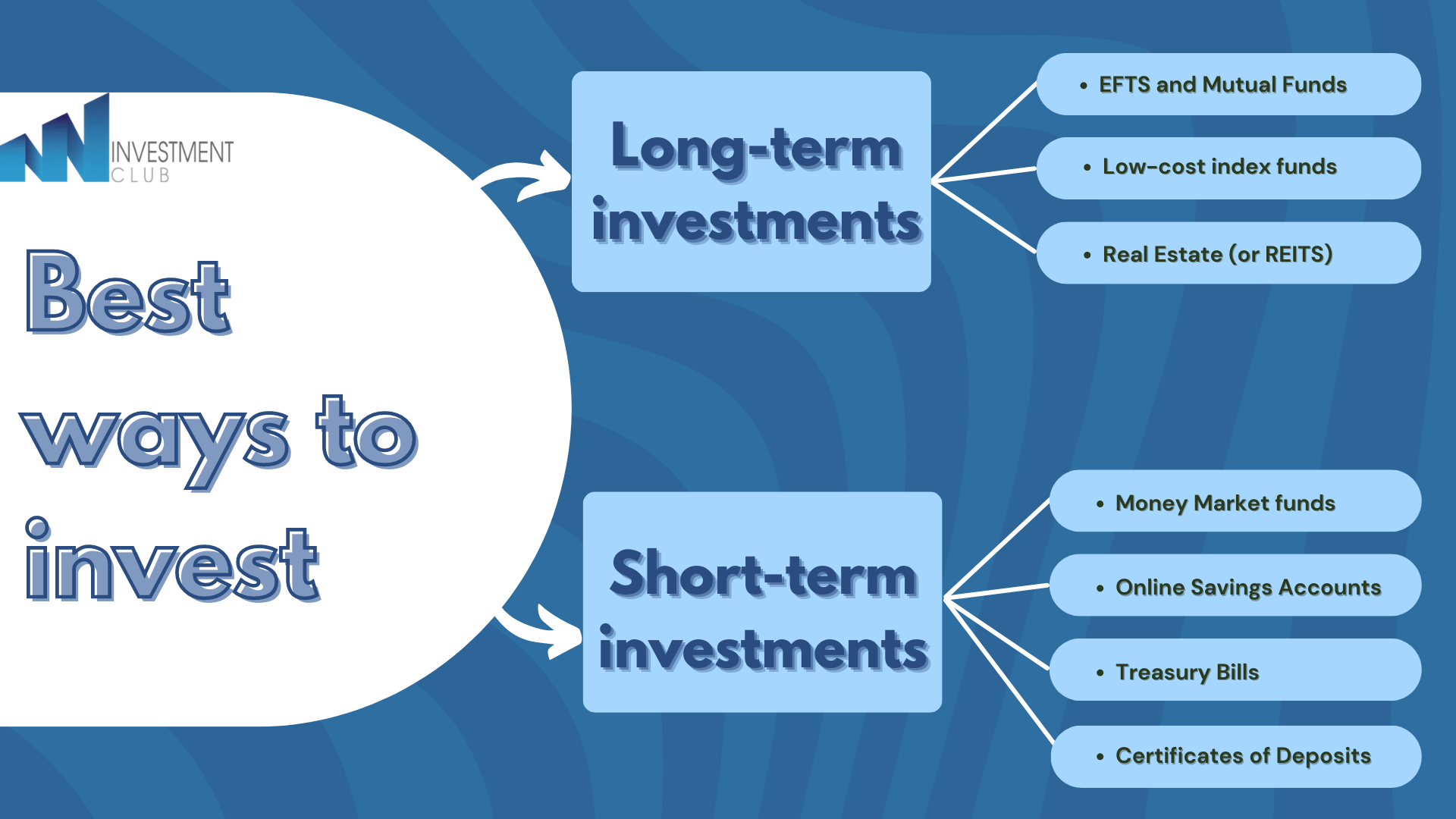

Best ways to invest

When it comes to investing, there are so many options that we don't know where to begin, so we see individuals who trade stocks, those who invest in index funds or mutual funds, and others who cling to and push cryptocurrencies, non-fungible tokens, and a world of digital assets as the best way to go. To grow wealth, owing to technology and the internet, there is a plethora of knowledge about personal financial management and investment to absorb these days.

All of this raises a fundamental question: What are the best ways to build wealth?

Importantly, there are several methods to construct a healthy investing portfolio utilizing stocks, bonds, mutual funds, real estate, and other assets. However, the best plan for you will be determined by how much additional money you have, your risk tolerance, and when you may need to access your money in the future.

How to Accrue Wealth Through Long-Term Investments: Diversification, proper asset allocation, and lots of time are all required for wealth creation. Here are some of the greatest methods to invest in order to create long-term wealth.

1- ETFs and mutual funds ETFs and mutual funds are funds comprised of a collection of comparable assets, such as stocks, bonds, commodities, or other sorts of assets. ETFs can be acquired or sold on a stock market, whereas mutual funds are normally purchased directly from the fund's management organization.

2- Low-cost index funds Index funds are often low-fee funds that track a benchmark index, such as the S&P 500.

3-Real estate (or REITs) Another excellent long-term investment is real estate. However, because investing in a main home often provides poor returns once costs and inflation are included, it is preferable to invest in publicly listed real estate investment trusts (REITs) for exposure to this asset class. REITs are a collection of income-producing real estate holdings that allow people to participate in real estate without actually owning specific buildings. Best of all, REITs allow you to invest in real estate through a taxable account or a retirement account without the burden and worry of being a landlord.

Short-term investments to secure your money: Short-term investments, in addition to long-term investments, can help you keep your money secure while taking advantage of compounding. Just keep in mind that "get rich quick" scams abound in the financial sector, so do your homework before putting your money at risk.

1- market funds Money market funds invest in short-term assets which can be quickly liquidated and are often obtained through an investment fund company.

2-Online savings accounts If you know you'll need money quickly, check for bank accounts you can create online. Although the predicted yield in today's interest rate environment is modest, a high-yield online savings account can assist keep your money secure in the near run. Because they do not have the overhead of actual bank offices, online savings accounts tend to provide competitive interest rates.

3-Treasury bills Treasury Bills are government-issued short-term financial instruments. They are regarded as among the safest investments since they are guaranteed by the government's full faith and credit.

4-Certificates of Deposit Lastly, consider CDs for your short-term savings or money that you might need to retrieve in the years ahead. Certificates of Deposit often give a greater interest rate than savings accounts since you are holding in your cash for a certain period of time ranging from three months to five years.

In brief, we present the graph below, which highlights the best investing approaches described earlier:

References:

https://arabhardware.net/articles/tips-manage-personal-finance- https://riyali.com/blog-

https://edition.cnn.com/cnn-underscored/money/best-ways-to-inves-money

Prepared by:

Shahad Alwahbi

Munira Alqaoud

Layan Adossary